Whereas the previous can’t assure future outcomes, it stays our most dependable useful resource for understanding market conduct. Beforehand, I outlined how Monte Carlo simulations can be utilized to estimate these possibilities. However relying solely on one methodology is limiting. Diversifying the methods we calculate possibilities provides robustness to the evaluation.

On this article, I’ll delve deeply into three extra strategies for calculating possibilities: Hidden Markov Fashions (HMM), seasonality-based possibilities, and implied possibilities derived from choices costs. Every methodology has distinct benefits and enhances the Monte Carlo method, offering a complete framework for assessing Credit score Put Spreads.

1. Hidden Markov Fashions (HMM): Unveiling Hidden Market Dynamics

Hidden Markov Fashions (HMM) are a classy machine studying method designed to research time-series information. They function on the idea that noticed information (e.g., ticker costs) are generated by an underlying set of “hidden states” that can not be immediately noticed. These states signify distinct market situations, resembling bullish developments, bearish developments, or durations of low volatility.

How HMM Works

-

Defining Observations and States:

- The noticed information on this context are the historic closing costs of the ticker.

-

The hidden states are summary situations influencing value actions. For instance:

- State 1 (Bullish): Increased possibilities of upward value actions.

- State 2 (Bearish): Increased possibilities of downward value actions.

-

State 3 (Impartial): Restricted value motion or consolidation.

-

Coaching the Mannequin:

- The HMM is skilled on historic value information to study the transition possibilities between states and the chance of observing particular value modifications inside every state.

-

For instance, the mannequin would possibly study {that a} bullish state is prone to transition to a impartial state 30% of the time, and stay bullish 70% of the time.

-

Making Predictions:

- As soon as skilled, the HMM can estimate the present state of the market and use this data to foretell future value actions.

-

It calculates the chance of the ticker being above a particular threshold on a given date by analyzing doubtless state transitions and their related value modifications.

Benefits of HMM in Choices Trading

- Sample Recognition: HMM excels at figuring out non-linear patterns in value actions, which are sometimes ignored by less complicated fashions.

- Dynamic Evaluation: Not like static fashions, HMM adapts to altering market situations by incorporating state transitions.

- Chance Estimation: For a Credit score Put Unfold, HMM supplies a probabilistic measure of whether or not the underlying will stay above the quick strike based mostly on historic market conduct.

By capturing hidden dynamics, HMM provides a extra nuanced view of market possibilities, making it a precious device for assessing threat and reward in Credit score Put Spreads.

2. Seasonality-Primarily based Chances: Unlocking Historic Patterns

Seasonality refers to recurring patterns in value actions influenced by components resembling financial cycles, investor conduct, or exterior occasions. In choices buying and selling, seasonality-based possibilities quantify how typically a ticker’s value has exceeded a sure share of its present worth over a particular time horizon.

Find out how to Calculate Seasonality-Primarily based Chances

-

Outline the Threshold:

-

The edge is expressed as a share relative to the present value (e.g., -2%, +0%, +2%). This normalization ensures the chance calculation is unbiased of absolutely the value stage.

-

The edge is expressed as a share relative to the present value (e.g., -2%, +0%, +2%). This normalization ensures the chance calculation is unbiased of absolutely the value stage.

-

Analyze Historic Information:

- For a given holding interval (e.g., 30 days), calculate the share change in value for every historic statement.

-

Instance: If the present value is $100, and the edge is +2%, depend how typically the worth exceeded $102 after 30 days within the historic information.

-

Combination the Outcomes:

- Divide the variety of instances the edge was exceeded by the full variety of observations to calculate the chance.

-

Instance: If the worth exceeded the edge in 70 out of 100 cases, the chance is 70%.

Purposes in Credit score Put Spreads

Seasonality-based possibilities reply the query: “In similar conditions, how often has this ticker remained above the breakeven?” This method is especially helpful for ETFs, which regularly exhibit extra predictable patterns than particular person shares. For instance, sure sectors would possibly carry out higher throughout particular instances of the yr, offering a further layer of perception.

Limitations to Take into account

- Seasonality possibilities rely fully on historic information and assume that previous patterns will persist. Whereas that is typically true for ETFs, it could be much less dependable for particular person shares or in periods of market disruption.

3. Implied Chances from Choices Costs: Extracting Market Sentiment

Choices costs are extra than simply numbers; they encapsulate the collective beliefs of market contributors about future value actions. By analyzing the costs of places and calls throughout numerous strikes for a given expiration date, we are able to derive the implied possibilities of the ticker being in particular value ranges.

Steps to Calculate Implied Chances

-

Gather Choices Information:

- Receive the bid-ask costs for places and calls at completely different strike costs for the specified expiration date.

-

Calculate Implied Volatility:

- Use the choices costs to derive the implied volatility (IV) for every strike. IV displays the market’s expectations of future value volatility.

-

Estimate Chances:

- For every strike, calculate the chance of the ticker being at or above that stage by utilizing IV and the Black-Scholes mannequin (or related strategies).

-

The chances are then aggregated to assemble a distribution of anticipated costs at expiration.

Why Implied Chances Matter

- Market Consensus: Implied possibilities mirror what the market “thinks” concerning the future, providing a forward-looking perspective.

-

Dynamic Changes: Not like historic strategies, implied possibilities adapt in real-time to modifications in market sentiment, resembling information occasions or macroeconomic information.

Utility to Credit score Put Spreads

For a Credit score Put Unfold, implied possibilities can reply questions resembling: “What is the market-implied likelihood that the ticker will remain above the short strike?” This perception helps merchants align their methods with prevailing market sentiment.

Conclusion

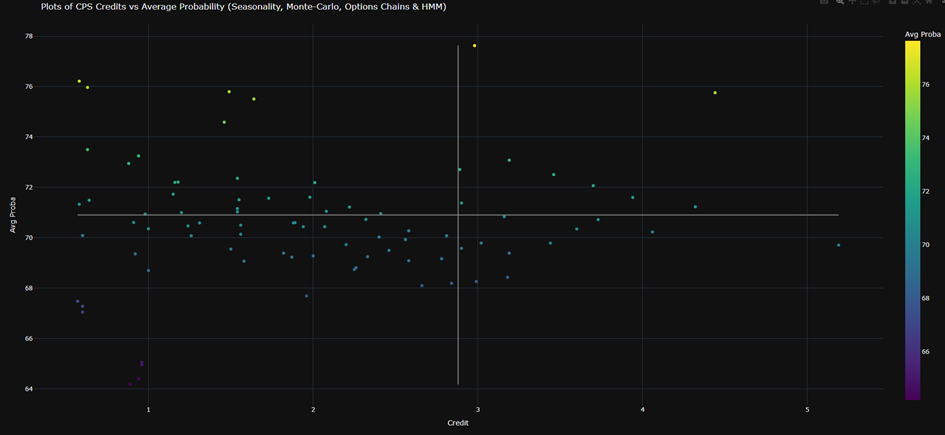

By integrating these three strategies—Hidden Markov Fashions, seasonality-based possibilities, and implied possibilities from choices costs—into my current Monte Carlo framework, I’ve developed a sturdy system for evaluating Credit score Put Spreads. This method allows a complete evaluation of Out-of-the-Cash (OTM) Credit score Put Spreads amongst a selection of ETFs, filtering for:

- Acquire/loss ratios inside particular thresholds,

- Expiration dates inside an outlined vary,

-

A minimal credit score of $0.50.

The result’s what I wish to name a “stellar map” of chosen spreads:

accompanied by a abstract desk:

These instruments present readability and actionable insights, serving to merchants determine one of the best trades—these providing the very best chance of success whereas maximizing potential returns relative to threat.

Trying forward, the subsequent step will contain calculating the anticipated worth ($EV) of those trades, combining possibilities and potential outcomes to additional refine the choice course of.

The final word objective stays the identical: to stack the percentages in our favor—not by predicting actual costs, however by estimating possibilities with precision and rigor.

Keep tuned as I proceed refining these strategies and increasing their functions!

{kind=link}